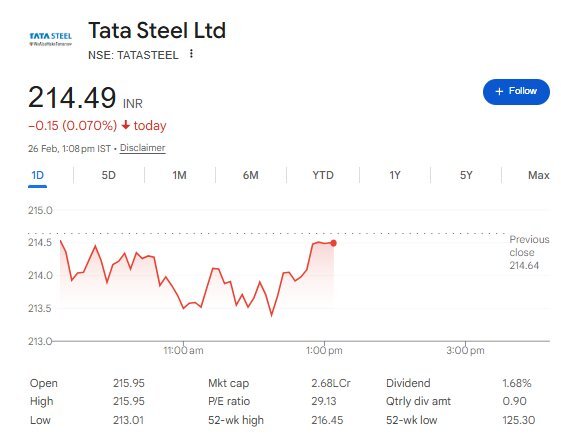

Mumbai News, 26 February 2026: The leading company in the Indian steel sector, Tata Steel Ltd, saw its shares start slightly lower in the market today. By 1 PM (13:00 IST), the company’s share was trading between ₹213.50 and ₹214.30 on NSE, showing a decline of about 0.50% to 0.54% compared to yesterday’s closing price of ₹214.64. A similar trend was seen on BSE, where the share was around ₹213.95 (compared to the previous closing of ₹214.65, down up to -0.33%).

NSE live updates (26 February 2026, until 1 PM):

- Opening price: ₹215.95

- Day high: ₹215.95

- Day Low: ₹213.01

- Current price: ₹213.49 (updated till 11:54 IST; later slightly recovered to around ₹214)

- Volume: More than 1.17 crore shares (traded value around ₹252 crore)

- VWAP: Around ₹214.40

- 52-week high: ₹216.45 (25 February 2026)

- 52-week low: ₹125.30 (April 2025)

BSE live updates:

- Current price: ₹213.95 to ₹214.30

- Day range: ₹213.05 to ₹215.90

- Volume: around 3.8 million shares

- Market cap: ₹2,66,500 crore to ₹2,67,520 crore

The metal sector in the market is overall in a positive mood. In the past few days, steel companies are benefiting from the safeguard duty imposed by the government to stop imports from China. Tata Steel’s shares have risen 10-12% in the past month, reaching a new 52-week high on 25 February. However, today there is slight pressure due to profit booking.

What do Dalal Street analysts and top brokers say?

After Tata Steel’s Q3 FY26 results (December 2025), brokers have raised target prices. The company’s consolidated net sales reached ₹57,002 crores (6.25% YoY growth), which has analysts feeling bullish.

- Motilal Oswal: Buy recommendation, target price ₹240. Around 12-14% upside from the current price. Focus on domestic demand, capacity expansion (NINL project), and improvements in the European business.

- JM Financial: Buy rating, target ₹240 (previously ₹215). Target raised as Q3 EBITDA exceeded expectations.

- MK Global (Emkay Global): Buy, target ₹230 (15% up). Prices are expected to rise in Europe due to carbon tax and protectionism.

- Systematix Institutional Equity: Buy, target ₹230. 15-25% upside potential in the metal sector.

- Consensus average (among 27 brokers): ₹212 to ₹235. Most brokers are giving Buy/Accumulate ratings. Some have set a short-term target of ₹233.

According to Trendline and other platforms, the average target is ₹212.78, which shows a slight dip from the current price, but the long-term outlook is strong due to Q3 results and the green steel policy in Budget 2026.

Technical analysis and market outlook

Technically, the share is strong at the ₹212 support. The breakout could happen at ₹217. According to analysts, steel demand is expected to rise by 6-9%, and with China’s supply discipline and domestic infrastructure boost, Tata Steel is likely to perform well in 2026. European operations are heading towards breakeven.

Conclusion

Tata Steel’s share has remained attractive for long-term investors. There might be volatility in the short term, but brokers are looking at a 15-20% upside. Consider your own risk appetite and market conditions before investing. Follow platforms like the NSE/BSE website for updates until the market closes.

Disclaimer:

(NiftySharePrice.com stock market news is based on publicly available authentic data sources like NSE – BSE and SEBI-authorized brokers & analysts only. Investing in the stock market involves risk. So, do your own research and consult your authorized advisors before investing.)